Moving to Salem Oregon insurance — here’s your checklist. Moving to Salem, Oregon? Don’t forget about insurance.

You need to update your policies in the first 30 days. Oregon has different requirements than most states. And getting it right saves you money and legal headaches.

Here’s your step-by-step insurance checklist for moving to Salem.

What Insurance Do You Need Before You Move?

Good news first. Your current out-of-state policy doesn’t expire the moment you cross the state line. Oregon recognizes what’s called an out-of-state clause — basically, your existing policy extends for a short grace period after you establish residency. That grace period is a bridge, though. It’s not a permanent solution, an

Here’s the actual timeline. Once you establish Oregon residency, you have 30 days to get your Oregon driver’s license, register your car, and switch to an Oregon-compliant policy. Miss that window and you’re technically out of compliance — even if you have a policy card in your glove box. Oregon can suspend both your registration and your license if you let it lapse. That’s a harder problem to fix than just making a phone call in week one.

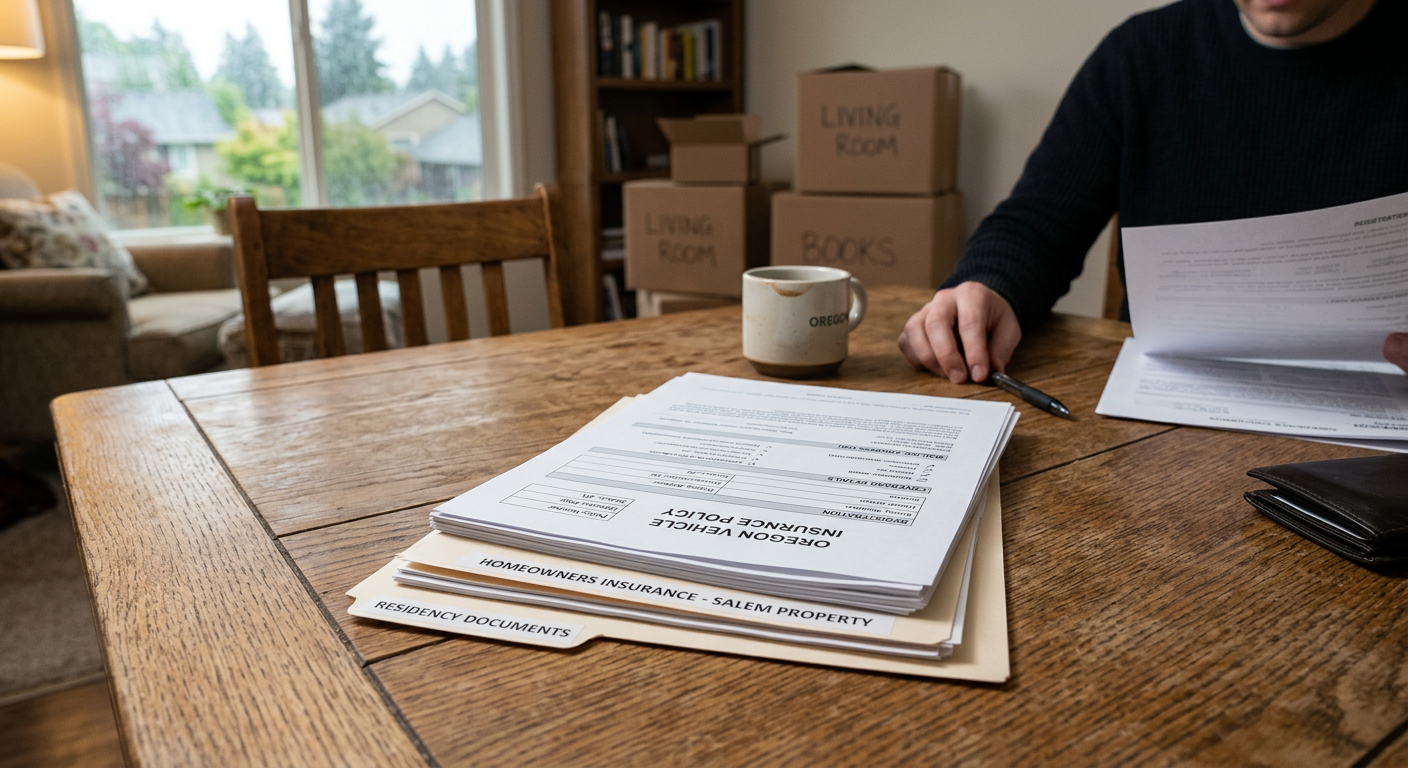

If you’re renting, ask your new landlord before you sign. Oregon law — specifically ORS 90.222 — allows landlords to require renters insurance as a condition of your lease. Most renters policies run $15 to $25 a month. That covers your furniture, your laptop, your clothes, and your liability if someone gets hurt in your unit. It’s a small line item with a lot behind it. Check out the renters insurance requirements in Oregon if you want the details.

If you’re buying, your mortgage lender will require proof of homeowners insurance before closing. That’s not optional — it’s part of the loan process. Get a quote early so it doesn’t hold up your closing date.

Either way, the 30-day window moves fast when you’re unpacking boxes and learning new streets. Start the process in your first week, before life gets busy. It helps to know what’s actually required so you’re not scrambling at the last minute.

Step 1: Know Oregon’s Auto Insurance Requirements

Oregon requires:

- $25,000 bodily injury (per person)

- $50,000 bodily injury (total per accident)

- $20,000 property damage

- Personal injury protection (PIP)

- Update your coverage to meet Oregon minimums

- Re-quote your policy (it may cost less or more)

- Send you a new proof of insurance card.

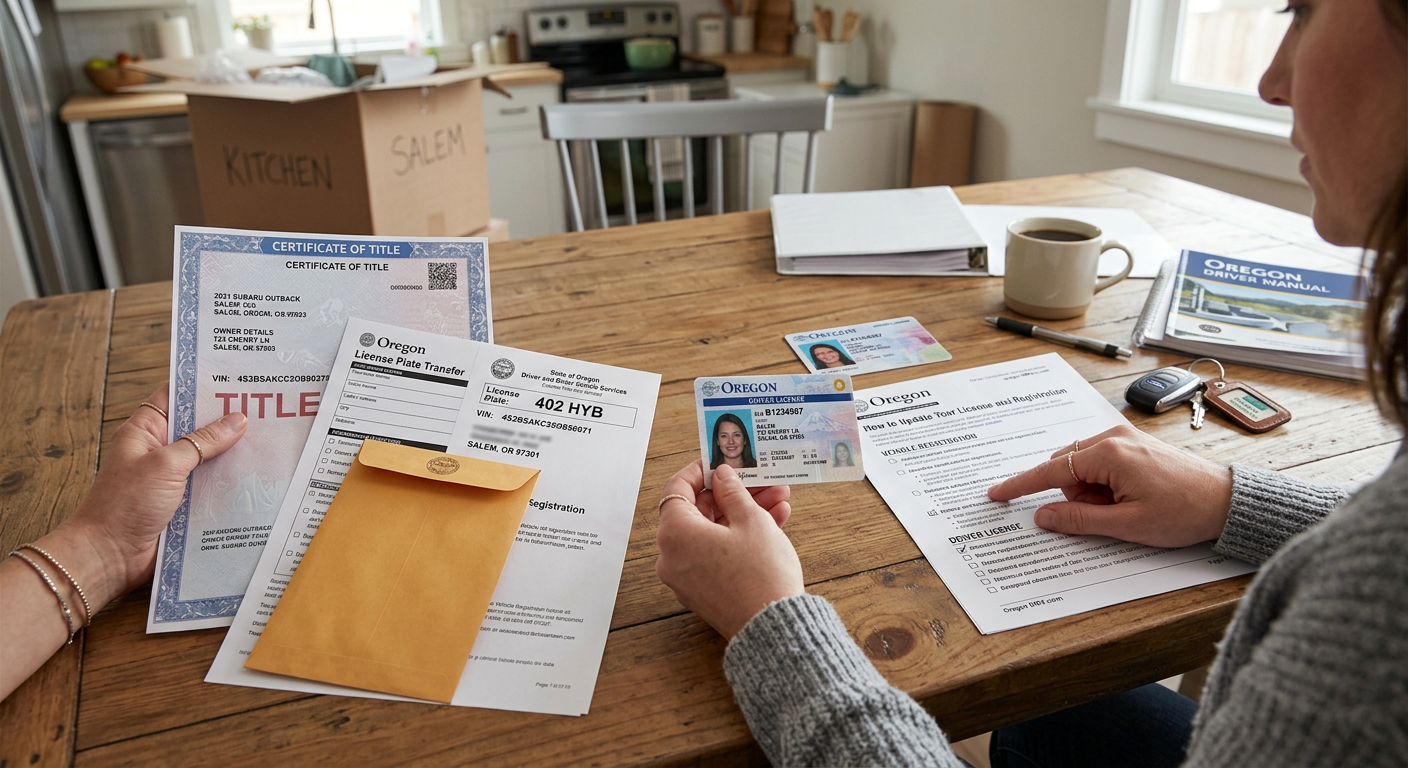

- Your old driver’s license

- Proof of Oregon residency (lease, utility bill, or bank statement)

- Proof of Social Security

- Proof of car insurance

- ☐ Update auto insurance to Oregon standards

- ☐ Get new Oregon driver’s license

- ☐ Register vehicle in Oregon

- ☐ Get renters or homeowners insurance

- ☐ Consider umbrella insurance

- ☐ Keep proof of insurance in your car

- ☐ Update your address everywhere (DMV, bank, employer)

Your out-of-state policy might have less. You need to upgrade within 30 days of moving. Here’s what Oregon car insurance actually requires — and what Salem drivers typically carry.

Step 2: Get Auto Insurance Before You Cross Into Oregon

Call your insurance agent (or get a new one — we’re in Salem!). Tell them you moved to Oregon and give them your new address.

They will:

Keep that proof in your car. You might get pulled over and need to show it.

Step 3: Update Your Driver’s License and Registration

Go to the Oregon DMV within 30 days. Bring:

You’ll get an Oregon license. Your old one expires.

Step 4: Register Your Vehicle in Oregon

You have 30 days to register your vehicle in Oregon. The DMV can do this when you get your license.

If your car is from California, you might not need DEQ testing here — Salem is outside the Portland metro area. Check with the DMV.

Salem Neighborhoods at a Glance

Salem is bigger than most people expect. And the neighborhood you land in affects more than just your commute — it can also affect your insurance rates.

South Salem is newer and suburban. It’s been growing fast in recent years. Lots of newer homes, good schools, a quieter pace. Auto and homeowners rates there tend to be pretty average for the city.

West Salem sits across the Marion Street Bridge in Polk County. It’s a different county entirely, which some insurers treat differently. Quieter streets, great views of the valley. Worth knowing before you assume your rates will be the same as the east side.

Keizer is technically its own city, just north of Salem. It has a close-knit, small-town feel even though it’s connected to Salem. Easy I-5 access and generally straightforward insurance rates.

Downtown and the Grant neighborhood are walkable and full of historic homes. Older construction means your homeowners policy needs to reflect actual replacement cost — not just market value. That gap can be significant, and it’s something a local agent will catch that an online quote tool often won’t.

North Salem is closer to I-5 and generally more affordable. Mixed residential and commercial streets. A good option if you’re watching your budget.

Each area has its own flood risk profile, housing stock age, and proximity to traffic. All of that feeds into what you actually pay. When you call your agent, tell them where you’re moving — not just that you’re moving to Salem.

The Insurance Stuff Nobody Tells You About Oregon

Oregon has a few insurance rules that catch new residents off guard. These aren’t small details — they’re requirements.

Oregon requires Personal Injury Protection, or PIP. Most states don’t have this. California doesn’t. PIP covers your own medical bills after an accident regardless of who caused it. So if someone rear-ends you, your own policy pays your ER bills while fault is still being sorted out. That matters a lot in the weeks right after a crash.

Oregon also requires uninsured motorist coverage. That’s more important than it sounds. A surprising number of drivers on Oregon roads are uninsured. If one of them hits you, uninsured motorist coverage is what protects you. Without it, you’d be going after someone who has nothing to go after.

Earthquake coverage is not included in standard homeowners policies. Oregon sits on the Cascadia Subduction Zone. Geologists have been warning about the potential for a major earthquake for years. Standard homeowners policies don’t cover seismic damage — not even close. If you want that protection, it’s a separate add-on. It’s at least worth asking about when you set up your policy.

Flood insurance is also separate. Salem has several waterways that flood in wet years — Mill Creek, Pringle Creek, and the Willamette River. FEMA flood maps determine your risk level. If your new home is near any of these, a standard homeowners policy leaves a significant gap. Take a look at the Salem flood insurance guide to see what applies to your address.

Step 5: Check Your Home Insurance Needs

Are you renting or buying?

If renting: Get renters insurance. It costs about $15/month and covers your stuff if there’s a fire, theft, or other damage.

If buying: Get homeowners insurance before closing. Your lender requires it. It covers your house and belongings if something goes wrong.

Step 6: Don’t Forget Umbrella Coverage (Optional)

If you own a home or have assets, consider umbrella insurance. It covers you if someone sues and your regular insurance doesn’t have enough.

It costs $100-300/year for $1 million in coverage. That’s cheaper than a lawsuit.

Your Insurance Checklist

Your First Call After You Arrive

One phone call handles most of this. (503) 390-5343 — that’s Sammons Agency, on Portland Road in Salem. One conversation covers auto, renters, and homeowners. You don’t need three different appointments.

They’ve been on Portland Road for 24 years. That’s not a call center. That’s a neighbor who knows Salem neighborhoods, knows Oregon law, and knows what coverage actually costs here versus what you were paying somewhere else.

If you prefer to speak Spanish, the team speaks it natively. Not transferred somewhere, not run through a translator — just a real conversation in the language you’re most comfortable with.

You can also start a quote before you even arrive. Head to sammonsagency.com and fill out the form. That way your coverage is lined up and ready when you pull into the driveway.

That’s it. You’re covered.

Have questions? Call us at (503) 390-5343 — we’re happy to help.

Start a quote online at sammonsagency.com or call (503) 390-5343.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, rates, and requirements may vary based on individual circumstances. Oregon insurance laws and regulations are subject to change. For personalized advice about your specific insurance needs, please contact a licensed insurance agent. Christian Sammons is a State Farm Insurance Agent licensed in Oregon, Washington, and California. State Farm, Bloomington, IL.

Leave a Reply