Your Kid Just Got Their License. Now What?

Teen driver insurance Oregon — getting your teenager licensed is a proud moment. It’s also the moment most Salem parents realize their auto premium is about to take a serious jump. That mix of pride and “oh no” is completely normal. Your teenager just passed their driving test, and now you’re staring down the reality that they’re going to be behind the wheel — alone — in Oregon rain, on I-5, maybe even through Salem during rush hour.

I’m Christian Sammons. I’ve had this conversation with hundreds of Salem parents. Adding a teen driver to your policy feels overwhelming until someone walks you through it. So let’s do that.

How Much Does It Cost to Add a Teen Driver in Oregon?

Let’s not sugarcoat it — adding a teen driver is expensive. Nationally, the average cost of full coverage for a 16-year-old is around $7,900 per year. In Oregon, you’re looking at a significant premium increase no matter how you slice it. Most Salem families see their auto bill climb anywhere from $1,500 to $3,500 per year after adding a teen, depending on the vehicle and coverage.

Why so much? Insurance companies look at the numbers. Teen drivers are involved in more accidents per mile driven than any other age group. That’s not a judgment call — it’s statistics, and it’s what drives the rate.

However, the good news: it gets better every year. By the time your kid hits 20, the rate drops considerably. And there are real ways to bring the cost down right now.

Oregon’s Graduated Driver Licensing Program — And Why It Matters for Insurance

Oregon’s GDL program is one of the more structured in the country, and for good reason: it works. But it also directly affects how insurers view your teen driver. Here’s what each stage means.

- Instruction Permit (age 15): Must hold for at least 6 months. Requires 50 hours of supervised driving, including 10 at night. Your teen cannot drive solo — a licensed adult must always be present. Most insurers don’t require you to add a permit holder to your policy, but call and confirm.

- Provisional License (age 16–18): No passengers under 20 for the first 6 months (unless family). No driving between midnight and 5 AM. This is statistically the highest-risk stage — most teen accidents happen here. Any violations during provisional can follow your teen’s record for years.

- Full License (age 18): All restrictions lifted. A clean provisional record going into a full license is a meaningful positive signal to insurers at renewal.

Each stage transition is a chance to revisit your policy. When your teen moves to a full license with no violations, bring that up when you call. It can affect your rate.

Keep Them on Your Policy — Don’t Let Them Drive Uninsured

This is the single biggest money-saving move. A standalone policy for a teen driver costs dramatically more than adding them to your existing family policy. We’re talking potentially double or triple the cost.

When you add your teen to your policy, they benefit from your driving history, your bundled home and auto discounts, and your established relationship with your insurance company. That history matters — and it saves real money.

Ways to Lower the Cost

Good Student Discount

If your teen maintains a B average or better (3.0 GPA), most insurers — including State Farm — offer a good student discount. For State Farm, that discount is typically around 7–10% off the teen’s portion of your premium. Bring in a report card or a letter from the school office. It’s paperwork that pays.

The discount applies to full-time students under 25. So it follows your teen into college, as long as the grades hold. Don’t forget to re-certify it each year at renewal.

Driver’s Education

Completing a certified driver’s education course can qualify your teen for an additional discount. Oregon requires driver’s ed for drivers under 18 anyway, so make sure you’re getting credit for it on your policy. Ask specifically — not every insurer applies it automatically.

Telematics — Drive Safe & Save

Usage-based insurance programs track driving behavior through an app or small device. State Farm’s Drive Safe & Save monitors things like speed, hard braking, rapid acceleration, and time of day. Safe driving habits earn real discounts — often 10–30% depending on the data.

For parents, there’s a second benefit: you can see how your teen is actually driving. Not their version of how it went. The data. If the numbers look good, you save money. If the numbers raise questions, you have something specific to discuss.

Choose the Right Car

The car your teen drives matters — a lot. Some vehicles cost significantly more to insure than others. Here’s what works in your favor:

- Older sedans with high safety ratings — Honda Civic, Toyota Corolla, Subaru Legacy. Reliable, affordable to repair, strong crash-test scores.

- Low horsepower — insurers rate high-performance vehicles as higher risk. A modest engine keeps the premium down and keeps temptations in check.

- No sports cars, no lifted trucks — even if they’re used and inexpensive to buy, they’re expensive to insure for a teen driver.

Before you buy that first car, call us and we’ll tell you what it’ll cost to insure. That conversation can save you thousands.

Bundle Your Policies

If you’re not already bundling home and auto insurance under one policy, this is a good time to look at it. Multi-policy discounts stack with other discounts — and adding a teen is a natural moment to review the whole picture.

Common Mistakes Parents Make

After 24 years helping Salem families with this exact situation, I’ve seen the same mistakes come up again and again. Here are the ones worth knowing before you make them.

- Adding the teen to the wrong vehicle. Parents sometimes list their teen on the household’s most expensive car — a newer SUV or a vehicle with high collision value. That spikes the premium unnecessarily. Match your teen to the least expensive vehicle they’ll actually drive.

- Skipping the umbrella policy. A teen in a serious at-fault accident can exceed standard liability limits fast. An umbrella policy adds a significant layer of coverage — often $1 million or more — for a relatively small annual cost. Many families don’t have one. They should.

- Not shopping multi-policy. If your home and auto are with different companies, you’re leaving money on the table. Combining them with one insurer almost always beats keeping them separate — especially when you’re adding a teen to the mix.

- Forgetting to formally add the teen. Some parents assume their teen is covered as a household member and never officially list them. If there’s an accident and the teen wasn’t on the policy, the claim can get complicated fast. Don’t assume — call and confirm.

What Coverage Do They Need?

Oregon requires at minimum:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $20,000 property damage

- Personal Injury Protection (PIP)

- Uninsured motorist coverage

But minimums are minimums for a reason. A teen driver in a serious accident can easily exceed those limits. We typically recommend higher liability limits and collision coverage for teen drivers — because the cost of being underinsured after an accident is far worse than the premium difference now.

What Happens If They Get a Ticket?

It happens. A speeding ticket or moving violation on a teen’s record can increase your family’s auto insurance cost significantly — sometimes for three to five years.

If it does happen, call us. There may be options — like a defensive driving course — that can help mitigate the impact. The worst thing to do is ignore it and wait for the renewal surprise.

When Do Teen Driver Rates Come Back Down?

The rate increase isn’t permanent. Here’s what actually triggers relief:

- Age 18: Full license, GDL restrictions lifted. A clean provisional period helps at the next renewal.

- Age 19–20: Accident rates drop sharply after age 18. Most insurers reflect that in the pricing.

- Age 21: Another meaningful step down. Many companies recalculate at this milestone.

- Age 25: For drivers with a clean record, rates normalize close to standard adult pricing by 25.

What actually moves the needle fastest: no tickets, no at-fault accidents. Age helps, but behavior drives it. A 22-year-old with a clean record pays far less than a 22-year-old with two tickets and a fender bender. That’s not speculation — that’s how the math works.

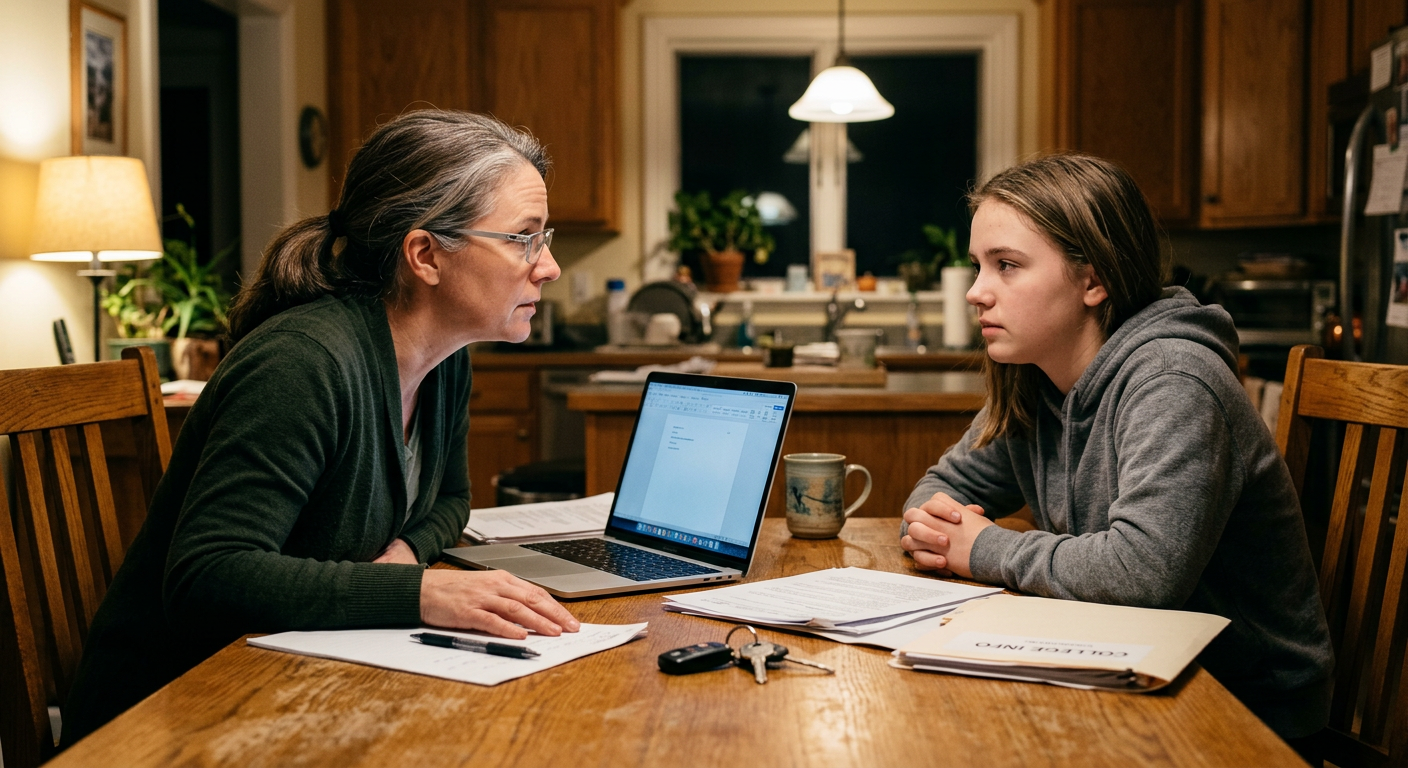

The Conversation to Have at Your Kitchen Table

Before your teen gets behind the wheel solo, sit down and talk about what’s actually at stake. Not just the rules — the real stuff. What happens financially if they cause a serious accident. What it means if they get caught driving without insurance in Oregon. Why a single reckless driving charge can follow them for years.

Make it real. Make it matter. And then make sure they’re covered properly so that when the inevitable minor incident happens, it’s an inconvenience — not a financial catastrophe.

Frequently Asked Questions

Do I have to add my teen to my policy as soon as they get their permit?

Oregon doesn’t require it during the permit stage since a licensed adult must always be in the car. But once your teen has a provisional or full license, most insurers require you to list them as a household driver. Call us when they get their permit and we’ll walk you through the timing.

What if my teen only drives occasionally?

Doesn’t matter. If your teen lives in your household and holds a license, they need to be listed on your policy — even if they “only drive sometimes.” An unlisted driver in an accident creates serious claim complications. Don’t leave that gap open.

Can my teen get their own separate policy?

Yes, but it will cost significantly more than staying on the family policy. Standalone policies for teens are expensive because there’s no driving history to offset the risk. The family policy is almost always the better financial choice until they establish their own record.

How long until our rate goes back to normal?

For most Oregon families, the biggest rate relief comes between ages 18 and 21, assuming no violations or accidents. By 25, most drivers with clean records are paying close to standard adult rates. A clean record is the fastest path there — more than any other factor.

We Do This Every Day

If you want to sort out the insurance question while you’re at it, Christian Sammons has been on Portland Road for 24 years. His team is bilingual. You can call (503) 390-5343 or go to sammonsagency.com — they’ll give you a straight answer.

Related Reading

- Car Insurance in Salem, Oregon

- SR-22 Insurance in Oregon: Complete Guide

- Driving Without Insurance in Oregon: The Real Cost

- Moving to Salem? Your Complete Insurance Checklist

Christian Sammons is a State Farm Insurance Agent in Salem, Oregon, serving the Willamette Valley since 2001. His office is at 4660 Portland Rd NE, #102, Salem, OR 97305.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, rates, and requirements may vary based on individual circumstances. Oregon insurance laws and regulations are subject to change. For personalized advice about your specific insurance needs, please contact a licensed insurance agent. Christian Sammons is a State Farm Insurance Agent licensed in Oregon, Washington, and California. State Farm, Bloomington, IL.

Leave a Reply